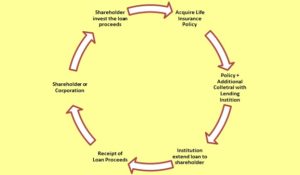

Whole life insurance is a type of permanent life insurance that provides coverage for the entire lifetime of the policyholder. In addition to providing a death benefit, whole life insurance also has a savings component, known as the cash value, which can be used for various financial goals, including funding a business.

Many successful entrepreneurs have utilized whole life insurance to fund their businesses and provide financial security for their families. Here are a few examples:

- Walt Disney Walt Disney, the founder of the Walt Disney Company, used his whole life insurance policy as collateral to secure a loan to start his first animation studio, Laugh-O-Gram Studio, in Kansas City, Missouri. When the studio failed, Disney moved to California and started his own animation studio, which eventually grew into the entertainment giant that we know today.

- J.C. Penney James Cash Penney, the founder of J.C. Penney, used his whole life insurance policy to borrow money to start his first store in 1902. He continued to use his policy as collateral to secure loans to expand his business, eventually growing it into a chain of department stores.

- Ray Kroc Ray Kroc, the founder of McDonald’s Corporation, used his whole life insurance policy to secure a loan to purchase the first McDonald’s franchise in 1954. He continued to use his policy as collateral to finance the expansion of the franchise, eventually turning it into the global fast-food behemoth that it is today.

- Sears Roebuck Richard Warren Sears, the co-founder of Sears Roebuck, used his whole life insurance policy as collateral to secure a loan to start his first watch business in 1886. He later used the policy to secure a loan to start Sears Roebuck, which grew into one of the largest department store chains in the United States.

- Frank VanderSloot Frank VanderSloot, the founder of Melaleuca, a wellness and personal care product company, used his whole life insurance policy to secure a loan to start his business in 1985. He continued to use his policy as collateral to finance the growth of his company, which now operates in over 20 countries and has over 5,000 employees.

- Nelson Nash Nelson Nash, the founder of the Infinite Banking Concept, used his whole life insurance policy as a way to finance his real estate investments in the 1970s. He discovered that he could borrow against the cash value of his policy at a low interest rate and then use that money to invest in real estate, generating a higher rate of return. This inspired him to develop the concept of Infinite Banking, which advocates using whole life insurance policies as a way to create a personal banking system and finance various investments.

- John D. Rockefeller John D. Rockefeller, the founder of Standard Oil Company, used his whole life insurance policies to create a family trust that would ensure his family’s financial security for generations to come. By using whole life insurance policies as a savings vehicle, Rockefeller was able to accumulate a significant amount of wealth that he could then pass down to his family through the trust.

- John Wanamaker John Wanamaker, the founder of Wanamaker’s Department Store, used his whole life insurance policy as collateral to secure a loan to purchase the building that would become his flagship store in Philadelphia in 1876. He continued to use his policy as collateral to finance the growth of his business, eventually building one of the largest and most successful department store chains in the United States.

- Jeff Rose Jeff Rose, a financial advisor and founder of Good Financial Cents, used his whole life insurance policy as a way to finance his business in its early stages. He discovered that he could borrow against the cash value of his policy at a low interest rate and use the funds to cover the expenses associated with starting his business.

Many famous entrepreneurs have used whole life insurance policies to finance their businesses, whether by using them as collateral to secure loans, as a savings vehicle to accumulate wealth, or as a means of creating a personal banking system. While whole life insurance may not be the right choice for everyone, it is a valuable tool that can provide entrepreneurs with the financial flexibility and security they need to pursue their goals and achieve success.